Have you heard a lot of hype about the 50-30-20 budget rule and how it helps to create a well-planned budget?

If yes, then the hype is worth it. The 50-30-20 rule allocates funds suitably for clearing debts, for needs, wants, savings, and investments, depending on your income.

You can begin using it by reserving 50% of the monthly income for needs, 30% for wants, and the rest 20% for savings.

You might be able to save more on needs or wants, and here’s where you can rotate the funds into savings. If the idea of budgeting in a simpler manner intrigues you, then you should try using the 50-30-20 rule.

This article will show how the 50-30-20 budgeting rules work to create a realistic budget. And, you can also find a FREE printable template and a FREE Google Sheets/ MS Excel Budget template at the bottom of the article.

So, read it to learn how this budget works, and enjoy the FREE 50-30-20 budget templates, which help you implement and track your budget effortlessly.

The No-BullSh*t Extra Money Apps To Join

Survey Junkie: Earn up to $50 per survey & a fixed $1.50 per referral. Sign up here.

Freecash: Get paid for taking surveys & testing apps. Earn up to a $250 signup bonus.

Swagbucks: Earn a $5 instant sign-up bonus & 10+ ways to earn real cash. Join now.

Branded Surveys: Paid over 35 Million. Earn up to $25 per survey. Sign up now.

Inbox Dollars: Get paid to watch videos. One has already made $75 within a week. $10 signup bonus.

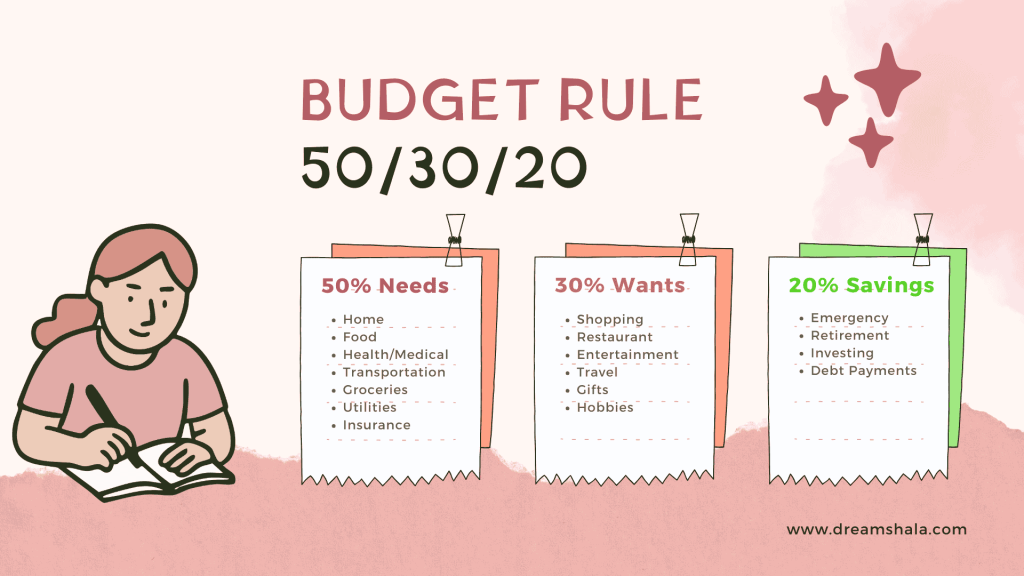

What is the 50/30/20 Budget Rule?

The 50/30/20 budgeting rule is the most popular fundamental that separates your pay into three categories.

It allocates 50% to your needs, 30% to your wants, and 20% to savings.

What Are The Three Categories of the 50-30-20 Budget Rule?

The three categories of the 50-30-20 rule are needs, wants, and savings.

The First 50%

This suggests allocating 50% of your after-tax income to your needs like rent, mortgage, groceries, transportation, basic utilities, child care, insurance, and minimum debt payments.

The Next 30%

Reserve 30% of after-tax income for your wants. You can spend this towards your vacations, concerts, restaurants, movies, entertainment, shopping, subscriptions, and luxury items.

The Last 20%

Allocate 20% of your after-tax income for savings. You can spend it towards cash savings, an emergency fund, debt payments, student loans, retirement, investments, and similar savings.

Such a budgeting rule helps you manage your money so you can use it for emergencies, retirement, and other savings plans as needed. The majority of people don’t need spreadsheets; you just need a notepad to prepare a breakdown.

It provides you with flexibility as you can divide all your savings into three categories.

How To Calculate the Percentage of The Budget?

Many people often remain confused about how much they should spend monthly. For example, if your monthly in-hand pay is $5000, then you calculate your budget by breaking it with the 50-30-20 rule.

Below is an example of how you can calculate with $5000:

- Needs $2500 (50%): To estimate the budget for your needs, you can calculate using $5000 × 0.50= $2500.

- Wants $1500 (30%): To calculate your budget for the wants, multiple $5000 × 0.30= $1500.

- Savings $1000 (20%): For calculating the budget you can allocate to savings, multiply it by $5000 × 0.20 = $1000.

Thus, for 50%, multiply the total in-hand income by 0.50, for 30% of wants, multiply by 0.30, and consequently by 0.20 for 20% savings.

Read Next: How To Sell Printables on Etsy? – Complete Guide

How To Deduct Taxes & Calculate The Net Income?

Firstly, you have to calculate the net income you get in your hands every month after tax deductions. Hence, it is known as after-tax income or net income instead of gross income.

To get a clear idea of your after-tax income, subtract all the taxes and pretax payroll deductions from your gross income.

For example, if you are an employee with a fixed paycheck, then this amount is specified on your paystub. Like an employer deducts retirement contributions, health insurance fees, and automatic savings, then you can add them back.

Besides, if you are self-employed, then deduct your business expenses plus the taxable amount from it to calculate your after-tax income.

If you are budgeting with your spouse or a partner, then add the two after-tax incomes together to prepare a household budget.

After calculating the monthly take-home pay, categorize the income into needs (50%), wants (30%), and savings (20%).

50/30/20 Budget Example With Taxes

Let’s understand budgeting adjustments. For example, your salary is $10,000 a month, and you pay 30% taxes on your monthly income.

You’ll get around $7000 in hand as your net income after taxes.

So, now, you have to divide your income as 50%, 30%, and 20% portions to adjust to this 50-30-20 budget rule. If we do the calculation part for the $7k net income, the numbers would come as…

- Needs(50%)= $3500

- Wants (30%)= $2100

- Savings (20%)= $1400

You might not like to spend more than $1000+ every month for rent or mortgage payments, especially if you have other needs like car payments, groceries, utilities, cell phone, etc., which is a must.

Accordingly, your needs can exceed 50% of your take-home pay, where you have to adjust the budget by rotating funds from wants to needs.

How To Budget Using the 50-30-20 Rule?

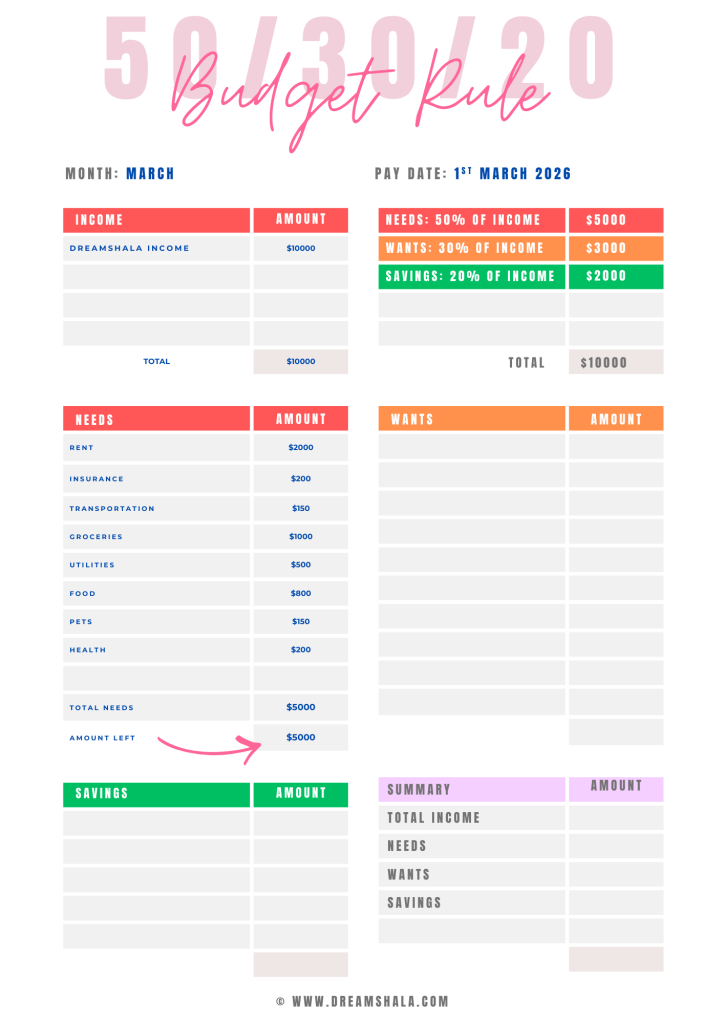

To budget your expenses using the 50-30-20 rule, use a pen and paper, or you can use a note-taking app for the purpose. I organise my finances using a note-taking app, while earlier I used a notepad.

You can also use our 50-30-20 Budget Rule Template for free. Just simply download the printable file and take a printout. You can use this sheet every month, both digitally and physically.

Credits: @dreamshala

Thus, the budgeting strategy becomes flexible. You can modify the percentages based on lifestyle and goals. For example, if you have debts to pay or want to allocate more for savings, then you can change the ratio to 50/20/30.

While you live in a region with high living costs, you might have to adjust the ratio to 60/20/20 so it suits your needs.

Below is a step-by-step guide of the same:

Step 1: Allocate 50% of Income to Your Needs

Now you have to jot down how much you spend on your needs. This is because these are fundamental living expenses and bills that are necessary for you to pay as needed.

Your needs can include the following:

- Rent or mortgage

- Groceries

- Food

- Insurance

- Healthcare

- Fuel

- Pets

- Utilities, etc.

Divide the income and fill the needs first into the template

If you want, you can also create sub-sections for each category. Besides, you can divide the Needs section into a “Monthly Bills” section and add your bills to it. Also, create a “Daily Essentials” section and add your needs to it.

The most important thing is to clearly differentiate between “needs” and “wants”. For example, buying groceries is a need, while wanting to eat in restaurants is a want.

Hence, using your own will to separate your needs and wants is essential. Typically, your needs should only cover the things without which survival is challenging.

You want to aim to spend 50% of your monthly after-tax income on your needs. These are necessary expenses that you can’t avoid; they can severely impact the quality of your life.

If you’re paying off credit card debt, you can’t forgo the minimum payment on your credit card because your credit score will be negatively impacted if you don’t pay the minimum.

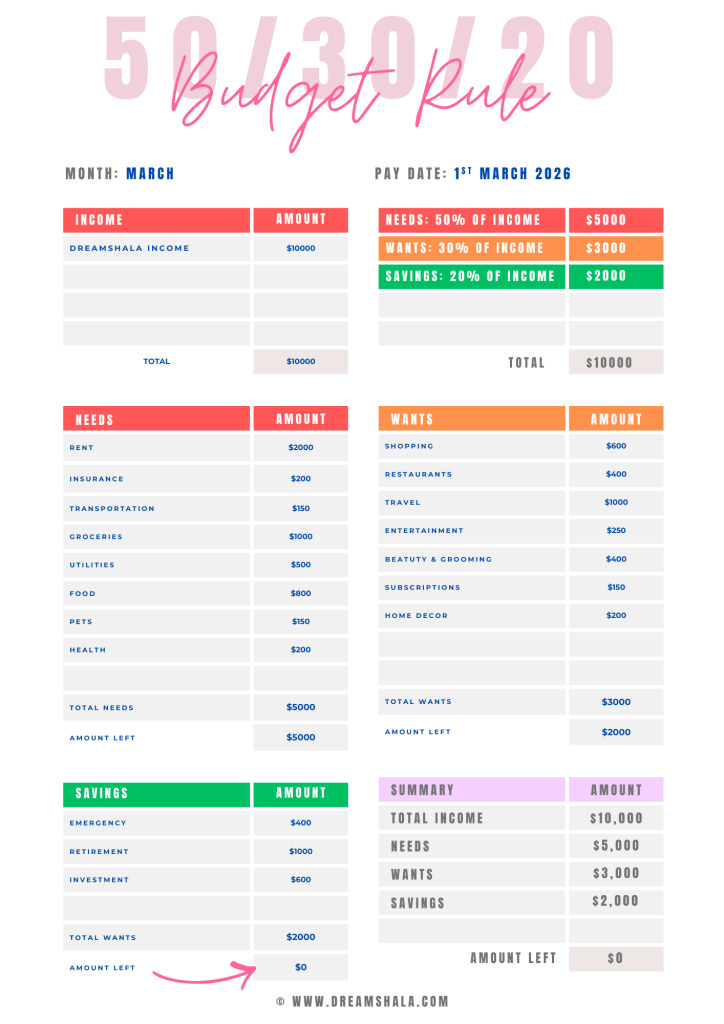

Step 2: Allocate 30% of Your Income to Wants

A vital step is to understand and determine the exact amount you are spending on your wants. This is because wants are extras and hence not always necessary for your livelihood or work.

You can jot down your wants on paper or in the “Wants” section of our 50-30-20-Budget Template, as shown in the picture below.

Fill the wants after filling the needs.

Having clarity about it can make a huge difference in your budget. This is because jotting it down helps you analyze the additional costs and helps you save money quickly or while clearing debts.

Though spending 30% of your income is a wiser idea, often not analyzing it adds up. Many times, you don’t even want to spend this much, but don’t realize that you are spending more on your wants than you think.

Some examples of your wants include a premium cell phone plan, Starbucks/Tim Hortons coffee, Netflix subscription, leisure travels, shopping, clubbing, gifts, long drives, etc.

These differ from person to person based on their lifestyles, and for some, even eating out can be a luxury, hence a need. These expenses are never fixed and vary every month.

For example, you might spend more in December on your wants due to Christmas and New Year’s, which includes gifting as well.

At the same time, it lowers over subsequent months but can be higher for any other aspect in another month. Thus, limit your expenses to 30% of your take-home pay.

Step 3: Allocate the Remaining 20% Income to Savings and Debt Payments

The next step is to make it a must and reserve 20% of your income for savings, debt payments, and investments.

You can prepare your savings in the “Savings” section.

Example of 50-30-20 budget rule with full budget allocation

You should have at least three to six months of living expenses as emergency funds with you. But if you don’t have any such funds right now, then start saving as $1000. Thus, you could stay prepared for any unplanned expenses without falling into debt.

After creating emergency funds, you can then use the 20% towards paying debts. If you have multiple debts, then pay the one that has the highest interest, as it will help you save a lot of money. It is known as the debt avalanche method.

After clearing the debts, you can use the 20% funds to save and invest.

The following is a list of some savings and debt repayment examples that you can add to 20% of your budget:

Short-Term Savings & Debts

- Clearing off credit card debts above the minimum payment

- Creating emergency funds

- Saving for home improvements

- Save up for an occasion, a wedding, a honeymoon, etc

- Saving up to buy a car

- Save it up for a home down payment

Long-Term Savings

- Saving to clear your mortgage amounts

- Save for retirement apart from deductions from your gross income

- Build funds for your children’s education through schemes like the 529 plan

- Save to begin a business if needed

Step 4: Adjust The Budget Plan and and Follow It

Irrespective of which budgeting plan you follow, always adhere to it strictly. This means beginning by separating your money based on the three categories of needs, wants, and savings.

Reserve 50% for needs, 30% for wants, and 20% for savings.

Once a week, use your spare time to understand your budget, understand your finances, and accordingly modify them as per your financial goals.

Nearly 30-40% of Americans use budgeting formulas but find it difficult to adhere to their categories.

Is the 50/30/20 budget rule good?

Yes, the 50/30/20 budget rule is suitable if you don’t like budgeting, as here you just have to categorize your expenses into three categories.

Pros of the 50/30/20 Budget

The 50/30/20 budget rule is ideal for those who have an average income and prioritize only three budgeting areas.

This is because using it, you can track your finances in a streamlined way without categorizing every expense singly.

So if you are someone who wants to save more money, then this budgeting rule is ideal. This plan is far better than not having a financing plan.

Thus, it is a good start to organize your budget.

Cons of the 50/30/20/budget

There are many who struggle to segregate “needs” and “wants”. For those, this structure can be difficult to reduce expenses.

Besides, if you live on a low wage, then your budget might not be suitable for these categories, as wants might take up the take-home pay more.

Even working youth living in expensive areas could not afford this budgeting rule, as it’s not feasible for their beginner-level income.

On the other hand, if you are a high-income earner, then it also won’t work for you. It is because you will want to allocate more funds for savings and investments instead of just 20%.

Thus, you should update your budget with time based on your financial goals, income, and lifestyle.

Other Popular Budgeting Methods

There are many more budgeting methods to consider instead of the 50/30/20 rule if you didn’t find it useful. Some of these methods are:

1. Zero-based Budget

The zero-based budget is my preferred method of organizing my finances. This is because here we assume that income minus expenses will be zero.

As you know, there’s a zero-based budget, so every leftover or take-home penny has a specific reserved task. For example, you might use some cash to pay expenses, and the rest you might distribute in savings, investments, or clearing debts.

2. Envelope Budget System

Dave Ramsey popularized this system, where you save and manage your monthly expenses in cash and envelopes. This also works without cash by reserving the amounts or via cards.

It is ideal for those who are learning budgeting.

3. Budget Calendar Method

The budget calendar method uses a calendar and tracks payment due dates, paychecks, bill tracking, and more dates in it. This gives you an idea of how much funding will flow in for a particular month.

Some important things you can add to the budget calendar include:

- Paydays

- Bills with due dates

- Saving contributions

- Investment dates

- Special events and holidays

4. 70/20/10 Rule Money

The 70/20/10 rule states that you should allocate 70% of your monthly budget towards needs, 20% towards wants, and 10% towards savings. It helps in regions with high living costs.

5. 60/30/10 Rule Budget

The 60/30/10 budget is also known as the 60/10/30 budget rule. Here, you should spend 60% of your income towards needs like living expenses, groceries, transportation, etc.

Next, allocate 30% of your income towards savings like emergency funds, savings, and extra debt payments.

Lastly, reserve the 10% for your wants, like leisure experiences.

6. 30-30-30-10 Budget

The 30-30-30-10 budget rule is another simpler one that divides your take-home pay into varied categories that lie in your budget.

- Spend 30% of monthly income for living expenses like rent/mortgage, appliances, transportation, etc.

- Use another 30% for your monthly income and other living needs like utility bills, groceries, internet, school needs, phone, and more.

- Allocate 30% of your pay for achieving your financial goals like clearing debts, saving for retirement, investing, and more.

- Reserve the remaining 10% for miscellaneous spending like streaming services, travel, entertainment, etc.

50/30/20 Budget Rule FAQs

1. Can you follow the 50/30/20 budget rule with irregular income?

Yes, you can follow the 50/30/20 budget rule with irregular income as well, since you just get paid in fragments at different intervals of the month, which you can combine.

2. Is the 50/30/20 rule weekly or monthly?

The 50/30/20 budget rule is a monthly rule that segregates income into needs, wants, and savings. But if you are paid biweekly, then create a budget sheet for every paycheck and follow the rule accordingly.

3. What is a good amount of money to have leftover after bills?

After following the 50/30/20 budget rule, you should have 50% of your income with you after bill payments. Here we assume that your needs and nearly half of your take-home monthly pay.

4. How much per paycheck should you save?

If you adhere to the 50/30/20 rule, then reserve at least 20% of the amount from your paycheck for savings, investments, and clearing debts.

5. Why is the 50/30/20 rule easy for people to follow, especially those who are new to budgeting and saving?

The 50/30/20 rule is easy to follow for novice budgeting as it categorizes all your funds into three parts for better simplicity and guidance.

50/30/20 Budget Rule – Free Templates:

As we promised, we are giving you these specially-designed budget templates for you absolutely for FREE.

You know many people charge $10 – $20 per template, but I’m not trying to capitalize on it.

But if you like these templates and found them useful, do me a favor by simply pinning this article to your Pinterest profile.

I truly appreciate your support, and it motivates me to create more helpful content and free templates for you.

50/30/20 Budget – Printable Template:

Download the 50/30/20 Budget Rule – Printable Template PDF here.

This template is for people who like to prepare a budget using pen and paper.

To use this printable template, you just need to download the PDF file and print it out on paper every month to divide your income following the budget rule.

It is super easy to use, as you can see that I’ve already explained in the above sections of this article. If you are doing it first, simply take a printout of this template and start following this article.

You can do it on your own from next month onwards.

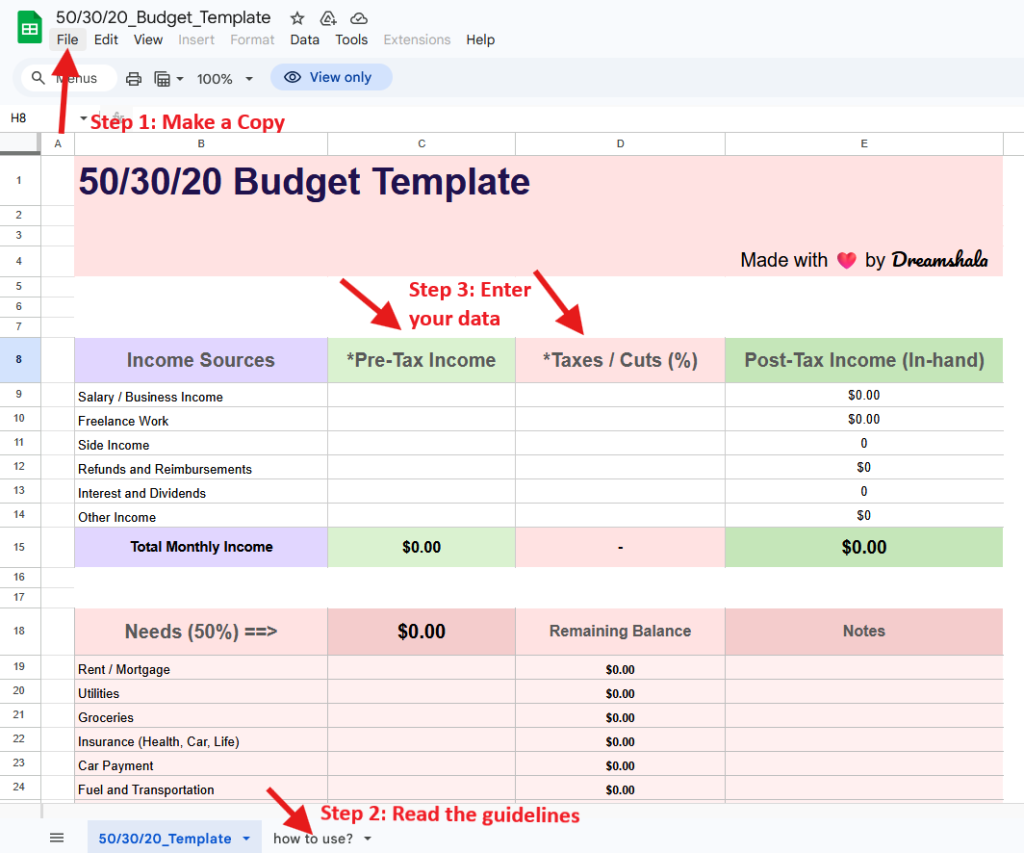

50/30/20 Budget – Google Sheets / MS Excel Template:

Access The 50/30/20 Budget Rule – Google Sheets/MS Excel Template here.

This Google Sheets / Excel Template is for those who want to plan and track their budget using their mobile, tab, laptop, or computer.

This template is completely automatic.

You just need to open the template using the above link, save it as a copy, and start using it by entering your data in the respective input columns as shown in the image below, and in the guideliness section in the template also.

Credit: Dreamshala

Don’t worry if you mistakenly enter data in the wrong fields and mess up the calculations.

You can always come back here and get a fresh copy of this template again and again.

So, don’t forget to Pin this article to your favorite Pinterest board now.

Happy budgeting.

Love from Dreamshala.

Shruti Gupta is a freelance writer and SEO specialist with extensive experience covering online income opportunities, digital tools, and personal finance topics. Since 2020, she has written hundreds of articles focused on helping readers find reliable ways to earn money online, start side hustles, and grow their income streams. Through her work at Dreamshala, Shruti aims to provide well-researched, transparent, and actionable insights that help people make informed financial choices in the digital economy.