With a limited income, do you hate waiting for a paycheck or payments at the end of the month for expenses that come up?

Well, most of you could relate to it, and budgeting gives you control over such cases.

This is because you can segregate your funds in an easy manner and accordingly plan the whole day without waiting for the next pay to sustain for the existing period.

Do you know that nearly 34% of Americans have $0 in savings? While this sounds scary, don’t become a part of it by avoiding budgeting.

The 70-20-10 rule is a forgiving one and helps you achieve financial goals without living from paycheck to paycheck.

In this article, we will not only teach you the 70/20/10 budget rule, but we will also provide the custom-made printable and Google Sheets templates for you without charging a penny.

So, in case you are struggling to make budgets, this article is definitely for you.

Keep reading and pin this article on Pinterest for future reference.

Need Easy & Extra $300/Mo For Free?

Survey Junkie: Earn up to $50 per survey & a fixed $1.50 per referral. Sign up here.

Freecash: Get paid for taking surveys & testing apps. Earn up to a $250 signup bonus.

Swagbucks: Earn a $5 instant sign-up bonus & 10+ ways to earn real cash. Join now.

Branded Surveys: Paid over 35 Million. Earn up to $25 per survey. Sign up now.

Inbox Dollars: Get paid to watch videos. One has already made $75 within a week. $10 signup bonus.

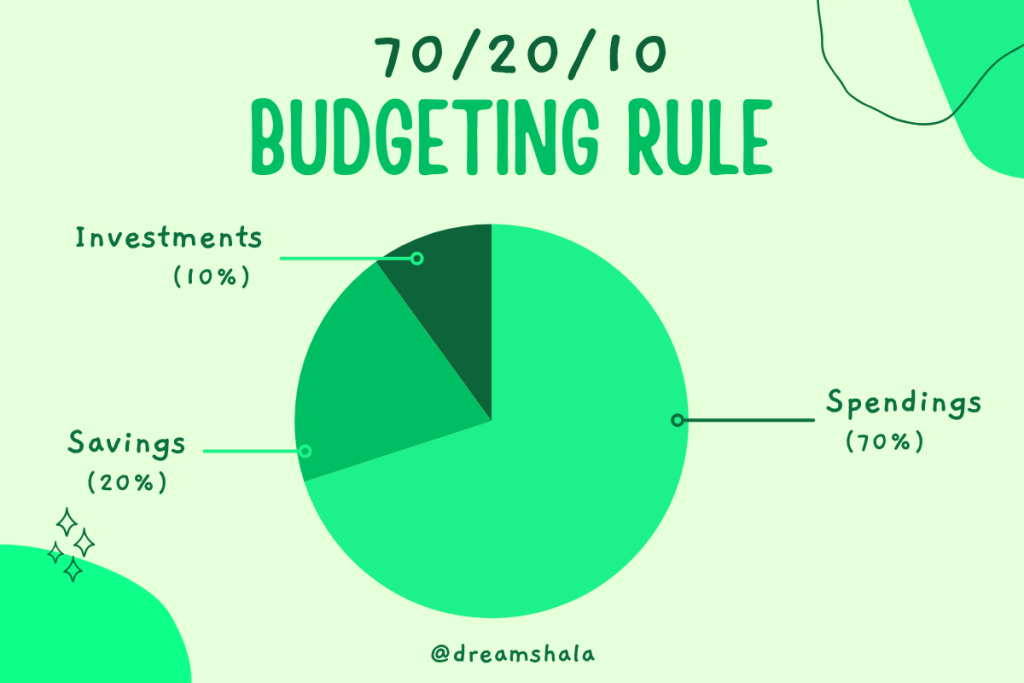

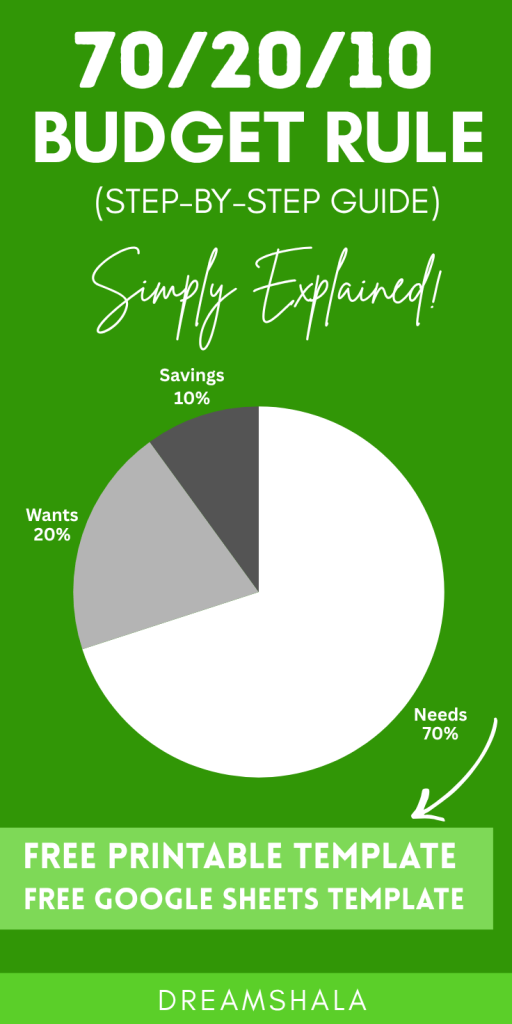

What is the 70/20/10 Budget Rule?

Just like other budgeting methods, like the 50-30-20 rule, the 70-20-10 budget categorizes your post-tax income into three categories.

- 70% of the income for monthly spending

- 20% of the income for savings

- 10% of the income for giving, investments, and additional debt payments.

You have to first allocate 70% of the after-tax income towards your fixed and variable expenses, and the next 20% depends on your savings. Besides, reserve the rest 10% for investments or donations.

Many people invest while others just keep saving, which are two different ways, yet it depends on your preferences and planning.

Here are some ways people use the formula:

- 20% for savings and 10% for paying debts

- 20% for savings and 10% for investments/donations

- 20% savings and debt repayments, and 10% for investments

- 20% for savings and debt repayments, while 10% for leisure tasks

I find the 20% allocation for savings and debts, with 10% for investments, is the most viable option.

70% of The After-Tax Income Is For Monthly Spending

Using the 70-20-10, you use 70% of your after-tax income for living expenses like needs, wants, and similar expenses that you need.

The following is a list of some common needs:

- Mortgage, rent, or minimum down payments

- Utilities like electricity, water, garbage removal, maintenance, etc.

- Insurance for car, health, life, home, etc.

- Car expenses

- Transportation and gas charges

- Phone and internet charges

- Groceries and confectionery

- Restaurants and dine-outs

- Entertainment

- Memberships and Subscriptions

- Clothing and shopping

- Personal care items like grooming, hygiene, pet care, childcare, etc.

- Travelling’s costs

- Medical expenses

- Gifting costs if you don’t want to reserve it under the 10% category

- Minimum payments for debts like those of credit cards, student loans, etc.

The 70-20-10 rule differs from other budgeting methods, like the 50-30-20 rule, in the fact that you don’t have to segregate your needs and wants into separate categories.

Yet, we recommend that you split the 70% expenses as fixed and variable costs.

Recommended Articles:

How to Start a Dog Treat Business at Home?

How To Sell Printables on Etsy? – Complete Guide

50-30-20 Budget Rule: How to Make a Realistic Budget?

Fixed vs. Variable Expenses

Your fixed expenses are those that don’t change in a particular period or month.

Yet, they owe the largest portion of your budget because they are usually for things like housing, utilities, insurance, car payments, transportation, etc.

Besides, some of you would have discretionary fixed expenses like a club or gym membership, Netflix, etc.

They are not your needs, and you can survive without them, but the bills are consistent every month, so you have to pay them regularly. Some of the common fixed expenses are:

- Rent or mortgage payment

- Utilities like water, electricity, and gas, some of which are variable based on usage

- Car payments

- Insurance, subscriptions, and memberships

- Childcare, Petcare, and medications

Your variable expenses are buying groceries, eating or drinking out, going shopping, travelling, etc., as their monthly costs differ every month.

Some of these are discretionary, and you can survive without them, while others, like groceries and medications, are needed. So, it is necessary to ensure you spend somewhat less than the after-tax income needed for it.

Some of the common variable expenses are:

- Groceries

- Commuting charges

- Dining out

- Entertainment and leisure activities

- Household and personal care products

20% of Your Income is for Savings and Debts

20% of your after-tax income should be allocated for the savings category, as it will help you with a successful future.

For many people, savings are an obstruction as they don’t have any money remaining for savings because they earn hand to mouth.

So, it becomes challenging to save money, and many of you would correlate it. Many can’t afford an unexpected $1000 cost with their savings, so they go into debt.

Here’s where the 70-20-10 budget rule helps you prioritize savings and helps you build an emergency fund. Consequently, you can work towards long-term savings goals.

But irrespective of your financial situation, you must make a financial goal of saving a decent portion of your income.

Some of the examples of savings categories include:

- Emergency fund

- Sinking funds for future expenses

- Capital to start a business

- Funds to buy a home/property

- Retirement contributions like for 401(k), IRA, Roth IRA

- College savings plans for your kids, like Custodial accounts and 529 plans.

Include an Emergency Fund in Your 70-20-10 Budget

If you don’t have an emergency fund, then first save up to $1000 for it, which can help you cover any unexpected expenses in the future.

After saving it up, most experts suggest you must grow it, so you have at least three to six months of funds to survive without work. But if your paycheck isn’t fixed based on your work, then having a larger emergency fund is necessary.

Sinking Funds for Future Expenses

These are the funds where you have to pay annually, like for Amazon Prime, Christmas, Easter, medical, etc.

Often, it can be something for which you consistently save, like buying a new car, going to a wedding, or taking a vacation. You can prioritize them as needed.

Debt Repayments

If you want to pay down debt, use this 20% category to allocate funds to high-interest debt like credit cards, debit cards, and loans. But it doesn’t imply that you spend less than 20% for it, as those debt payments are also present in the 70% category of pay.

If any debt is costing you a lot financially, then prioritize clearing it first. Finding the correct debt clearance method is essential for it.

1. Debt Snowball Method

It targets debts with the lowest balance first. It means you pay for the minimum monthly debts, then reserve extra money for the ones with the smallest balance.

Thus, the order of repayment is smallest to largest, irrespective of interest rate. It gives you the motivation needed for quick wins and to save up for the long term.

2. Debt Avalanche Method

In the debt avalanche method, you clear debts with the highest interest rate first.

This means pay your monthly minimum debts, then save up to clear the debts based on the highest interest rate to the lowest order.

Thus, you save a lot, hence you can clear debts faster. As you clear debts faster, you save huge amounts of money overall.

10% of Your Income for Giving and Investments

Allocate 10% of your take-home income for investments. Finding the correct investments helps you build wealth and fulfill huge financial goals, especially with compounding.

Some examples include:

- Investment in stocks and bonds

- Cryptocurrency investments

- Real estate, ETFs, or mutual funds

Otherwise, you can even donate your 10% of income to charity or organizations you feel passionate about.

Many even give their 10% of funds to their preferred place of worship. However, giving is completely optional.

How to Follow the 70-20-10 Budget Rule?

Follow the 5-step procedure to create a personal budget with the 70-20-10 rule.

Step 1: Calculate Your After-Tax Income

Calculate your monthly take-home pay, also known as net income, instead of gross income.

For calculating after-tax income, subtract any taxes, pretax payroll deductions, or business expenses from the paycheck or money earned. Track it under the “Income” section.

If you are budgeting with a partner, then combine your net income and use your after-tax income together for budgeting.

For example:

If your or your family’s combined monthly income is $10000 per month, and you have to pay 40% to taxes, then your net income would be $10000 – $4000 (40% tax) = $6000 (take-home income)

So, first, clearly know your gross income and tax figures to continue with the budget.

After calculating the monthly take-home pay, segregate it into three categories:

- Living expenses (70%)

- Savings (20%)

- Investments (10%)

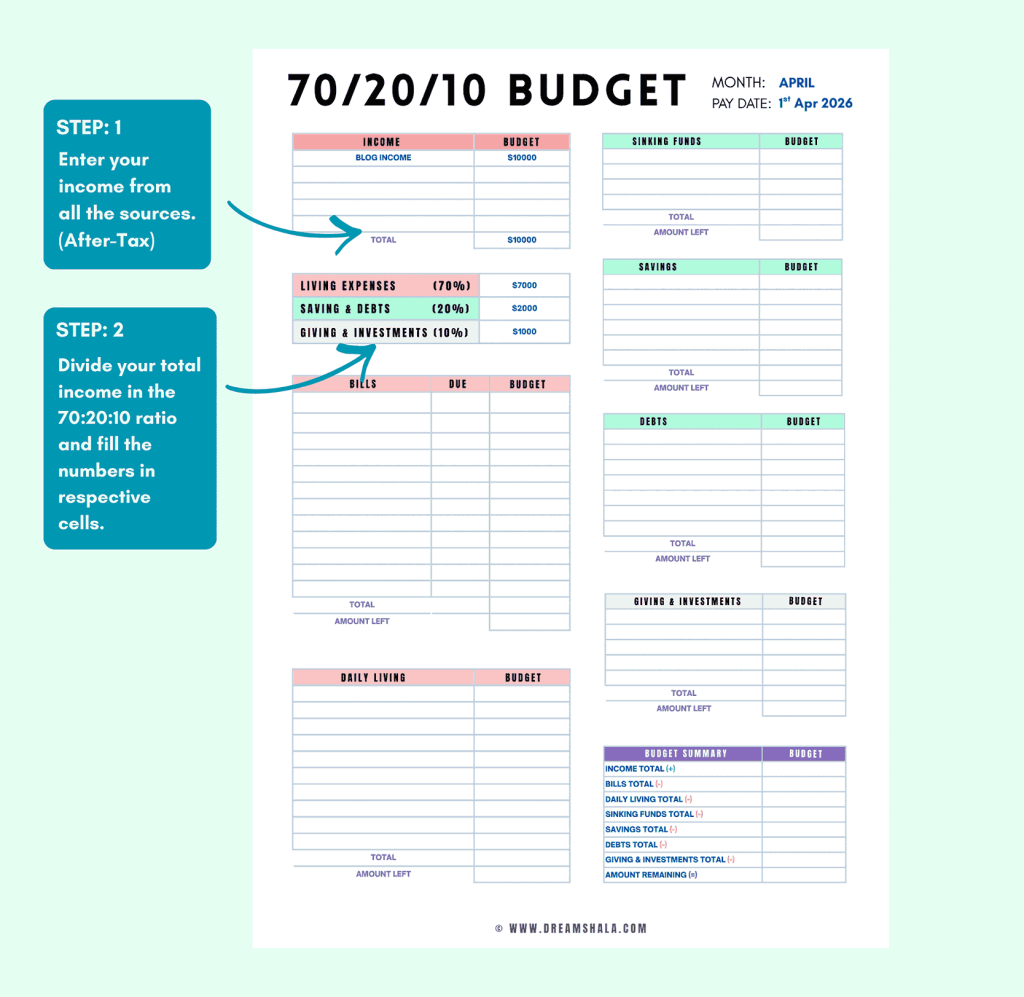

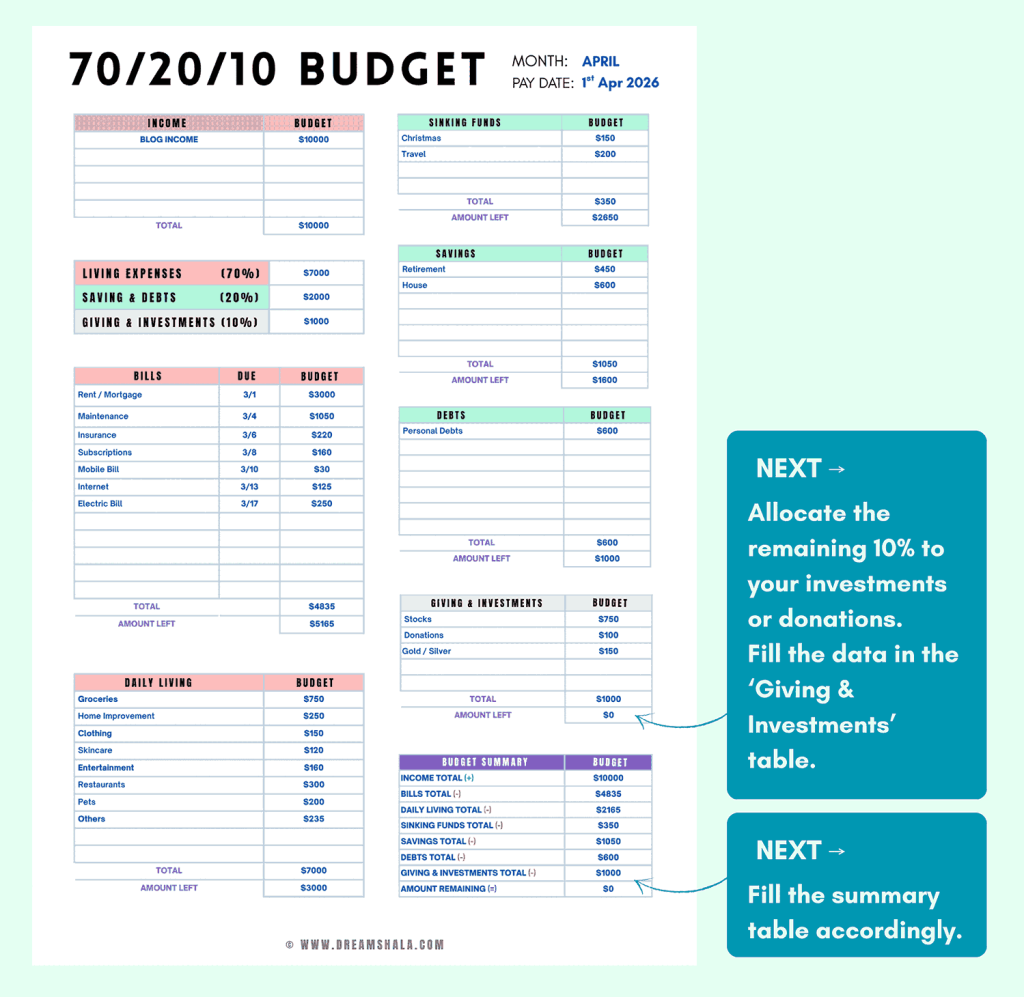

Follow the next steps to see how we did our budget using our 70/20/10 Budget Template. We not only help you understand it but also give you our custom-designed template for free to use for your monthly budgeting.

Credit: Dreamshala

You can download FREE Printable and Google Sheets Templates at the end of this article.

When you are ready with the printout, start your budgeting by filling in the details of the month, start date, and after-tax income from sources in the “Income” section.

Then, below the Income section, you’ll have a color-filled table where you need to fill in the amounts in 70%:20%:10% ratio.

Step 2: Jot Down Your Living Expenses

Further, figure out the funds that you currently have to use for fixed and variable expenses.

While budgeting on the printable, write bills and expenses in the “Bills” column. Further write other living costs and variable expenses in the “Daily Living” column.

Credit: Dreamshala

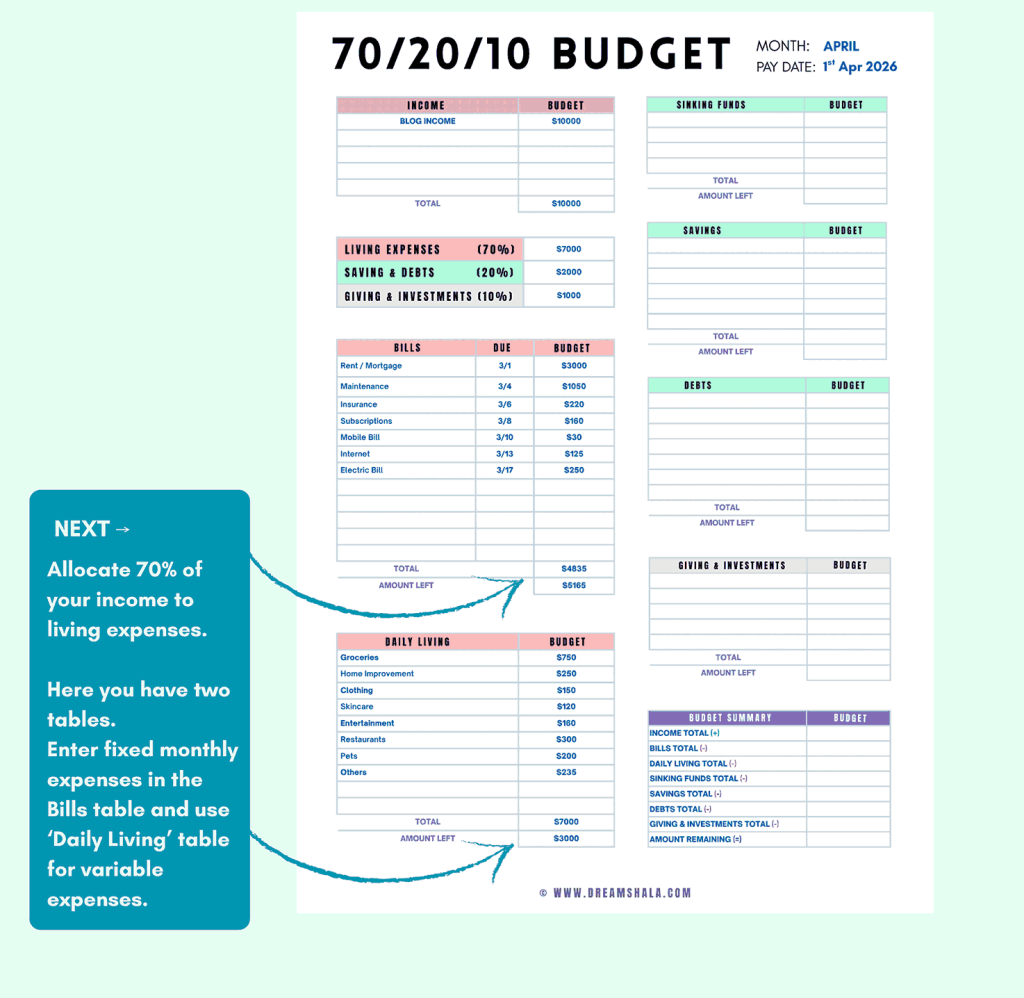

Make a target to spend 70% of your monthly after-tax income on your living expenses.

This can be for anything you spend during the month, and even minimum payments on debts.

If you are unsure of your expenses, then check your credit card and bank statements for the past 3 months and create an average to figure out the estimated expenses.

These would differ from person to person based on your lifestyle and your willingness to sacrifice.

For example, in one month you would spend a higher amount on gifts, while in the next month you could spend more on entertainment.

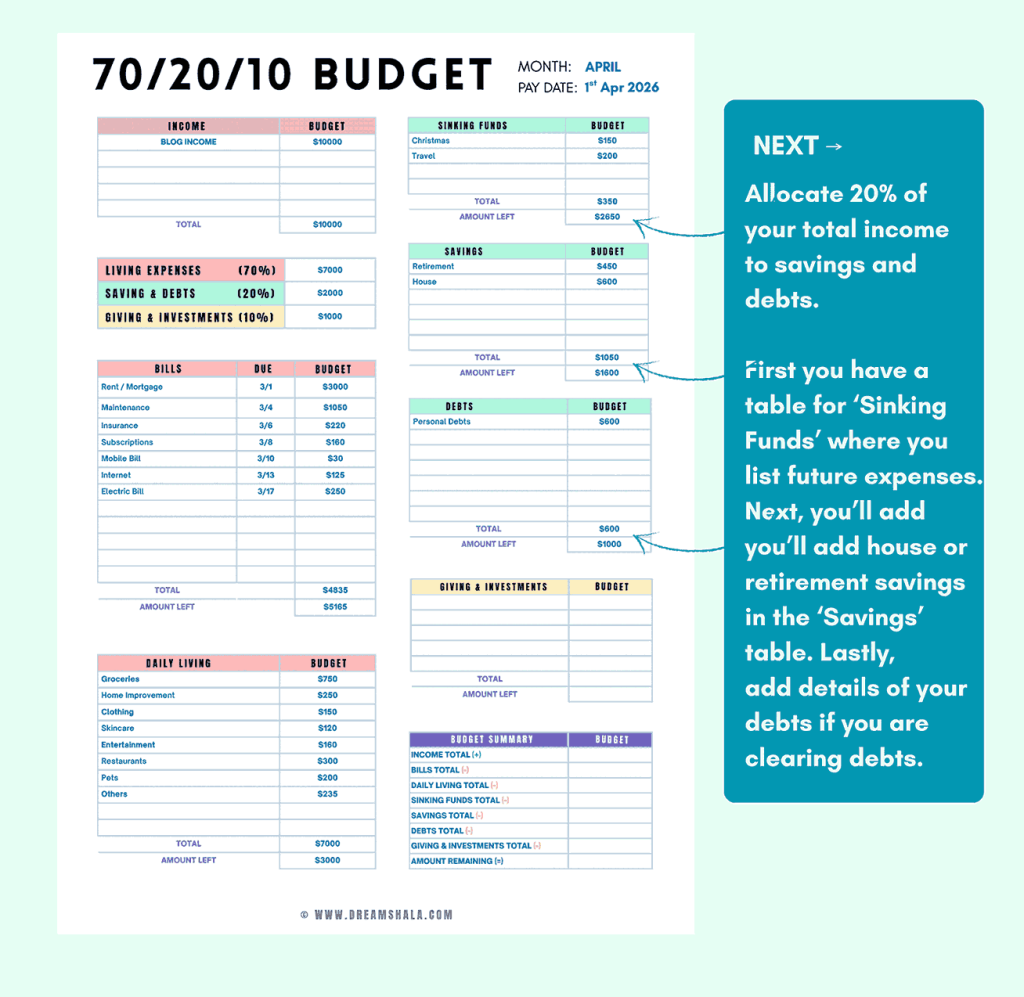

Step 3: Reserve Money for Savings and Future Expenses

As a next step, reserve 20% of your income for savings and debt payments.

In the note, note the sinking funds under the “Sinking Funds” section. Next, note your savings and debts in their respective columns.

Moreover, minimum payments of debts should be from the 70% expenses section.

And extra payments to reduce debts will go towards the 20% “savings” category.

Credit: Dreamshala

The tip to be successful with it is to get clarity on the WHY of your budget and accordingly set financial goals. Thus, you can stay motivated, consistent, and adhere to the budget.

Some common financial goals are creating an emergency fund, clearing debts, saving for retirement, saving for a down payment for a house/car, investing for college education, saving for a wedding, a dream vacation, or similar.

With a thorough understanding of your income and expenses, you can set realistic financial goals.

This is because you have awareness of how much money you can allocate towards it, or figure out ways to reduce expenses to achieve goals faster.

Suppose you are living from paycheck to paycheck, then saving 20% or investing 10% of it might be impossible, and you don’t need to bother. Just relax, take a deep breath, and know you are doing the best you can.

The 70-20-10 rule just helps you plan budgeting, and if you spend more than 70% of your income on living expenses, then that’s alright.

Even when I had begun my personal finance journey, the majority of my take-home pay was towards living expenses, and hence, I had little money for savings.

Though it is not easy, the key is to try to set aside whatever you can to deposit in a savings account.

Even though I sacrificed a lot and reduced my variable expenses to make it happen, my income and savings both grew.

Step 4: Invest or Donate 10% of Your Income

Keep aside the remaining 10% of your income for investments or giving, and decide how much you want to spend from it.

The uniqueness of the 70-20-10 rule is that, unlike other plans, it does recognize investment/donation factors. So, you can prioritize your savings, debt repayments, and investments based on your goals.

Credit: Dreamshala

For example, if you don’t owe any debt, then allocate 20% for savings and 10% for investments.

Besides, if you can go an extra mile, then you can include giving in the 70% section, keeping 10% solely for investments.

Step 5: Track The Expenses and Make Adjustments as Needed

Bravo! You are already on the path to take control of your finances and are doing great for it. To ensure that the budget works for you, track your spending after the month begins.

Thus, you could analyze how much you adhere to the budget and the amount you have left to spend in every budget category.

When you track your expenses, it gives you a sense of control over your finances.

You don’t worry if you have funds for groceries, as you always have a plan in advance and can stick to it.

Another good way to track your expenses is to find an easy method that is workable for you. For example, you can use a note-taking app or our monthly expense tracker as shown below.

Credit: Dreamshala

I personally use spreadsheets to track and manage my monthly expenses. So, every time I spend money, I record my transactions on the worksheet.

You can include your fixed and variable expenses plus debt payments under separate or the same sections based on your preferences.

Highlight every spending with a different color.

Thus, you can organize everything and figure out exactly how much money you spend on the villa, clothing, groceries, restaurants, etc.

Tracking your expenses also reveals any spending issues you have and can help you stay vigilant.

For example, in my initial phases of budgeting, I didn’t know the amount I was spending on fancy restaurants and clothing.

You might find it difficult to stick to the budget, but don’t feel discouraged; it might take some trial and error.

How to Know If The 70-20-10 Budget is Right for You?

Just like the 50-30-20 rule, the 70-20-10 budgeting method is an excellent option if you are new to budgeting.

I prefer the 70-20-10 method over the 50-30-20 method because you don’t have to separate your needs and wants. So, you categorize all your expenses in the 70% category.

It helps further if you have a lot of expenses, as you don’t have to do allocation based on fixed percentages.

Rather, you just have to focus on segregating it into 70% living costs, 20% savings, and 10% investments.

Besides, if you work for social causes, then the 70-20-10 rule is more lucrative as it has a separate category for donations.

But before giving socially, it is mandatory to have financial stability.

After you are comfortable financially, you can give back to others.

Thus, the 70-20-10 rule is ideal for those who:

- Budgeting novices

- Prioritize savings or pay down debts

- Need a simpler budgeting method

- Have a huge chunk of individual expenses

- What to give back socially

Advantages of the 70-20-10 Budget

One of the significant benefits of the 70-20-10 budget is that it’s quite simple to manage finances.

After you separate your take-home income into three categories of spend, save, and share, you are free to spend the way you want.

Besides, if you stick with the 70-20-10 rule, then you don’t have to worry about overspending or damaging your savings goals or debt payoff plans.

It is more forgiving than other budgets as it gives you guidelines about how to organize your money.

Further, when it’s about spending 70% of your income for living expenses, divide the spending categories in any way you want.

Pros of the 70-20-10 Budget Rule

- It is easy to use

- It is more forgiving than other budgets

- Helps you prioritize savings, debt payoff plan, and investments

Disadvantages of the 70-20-10 Budget

Personal finance is personal, and the 70-20-10 budget does not work for everyone.

Though it is a viable option for new budgeters, you should remember to try to make it workable for you.

The rule is a basic guideline, and you must consider your lifestyle and goals for it.

For example, if you live paycheck to paycheck, then you would juggle to save 20% of your take-home income or 10% for giving and investments.

So, it is ideal for those who can allocate 30% of their funds for purposes beyond living expenses.

For those who spend less than 70% comfortably, then allocate larger funds for paying debts, savings, and investments.

Though people prefer the simplicity of the 70-20-10 rule, others live better with detailed budgeting methods.

Thus, the overall goal should be the goal you want to achieve instead of living in a framework that isn’t suitable for you.

Besides, it doesn’t even segregate needs and wants, so it is complicated to identify your essential vs non-essential costs, hence you can’t improve it.

Cons of the 70-20-10 Budget Rule

- Saving 30% of the take-home income is complex for many households

- It does not separate your needs and wants

- Many prefer a detailed budgeting method

For example, let’s assume you are a single professional living in Austin, Texas, in the hybrid work setup and earn an average salary of $72,000 per year.

After taxes and deductions, your monthly net income becomes $4600 approximately.

With the 70-20-10 rule, your budget looks like:

- 70% living expenses: $3,220

- 20% savings: $920

- 10% investments: $460

This budget is in accordance with the 70-20-10 rule.

You can either combine all living expenses together or distribute them as fixed and variable expenses for better tracking and control.

For simplicity, I have used basic spending categories, but you can be more specific.

Alternative Budgeting Plan: 50-30-20 Rule

If you find the 70-20-10 rule overly restrictive or not aligning with your needs and goals, then the 50-30-20 rule provides a balanced approach.

The 50-30-20 budgeting plan segregates your after-tax income into 50% for needs, 30% for wants, and 20% for savings or debt repayment.

You can sustain it while ensuring financial stability if you can identify your needs and wants.

But it does not provide a separate allocation for investments and is mostly considered under the 30% savings.

70/20/10 Budget Rule – Free Templates:

As we promised, we are giving you these specially-designed budget templates for you absolutely for FREE.

You know many people charge $10 – $20 per template, but I’m not trying to capitalize on it.

But if you like these templates and found them useful, do me a favor by simply pinning this article to your Pinterest profile.

I truly appreciate your support, and it motivates me to create more helpful content and free templates for you.

50/30/20 Budget – Printable Template:

Download the 70/20/10 Budget Rule – Printable Template PDF here.

Also, download the Monthly Expense Tracker Template PDF here.

This template is for people who like to prepare a budget using pen and paper.

To use this printable template, you just need to download the PDF file and print it out on paper every month to divide your income following the budget rule.

It is super easy to use, as you can see that I’ve already explained in the above sections of this article. If you are doing it first, simply take a printout of this template and start following this article.

You can do it on your own from next month onwards.

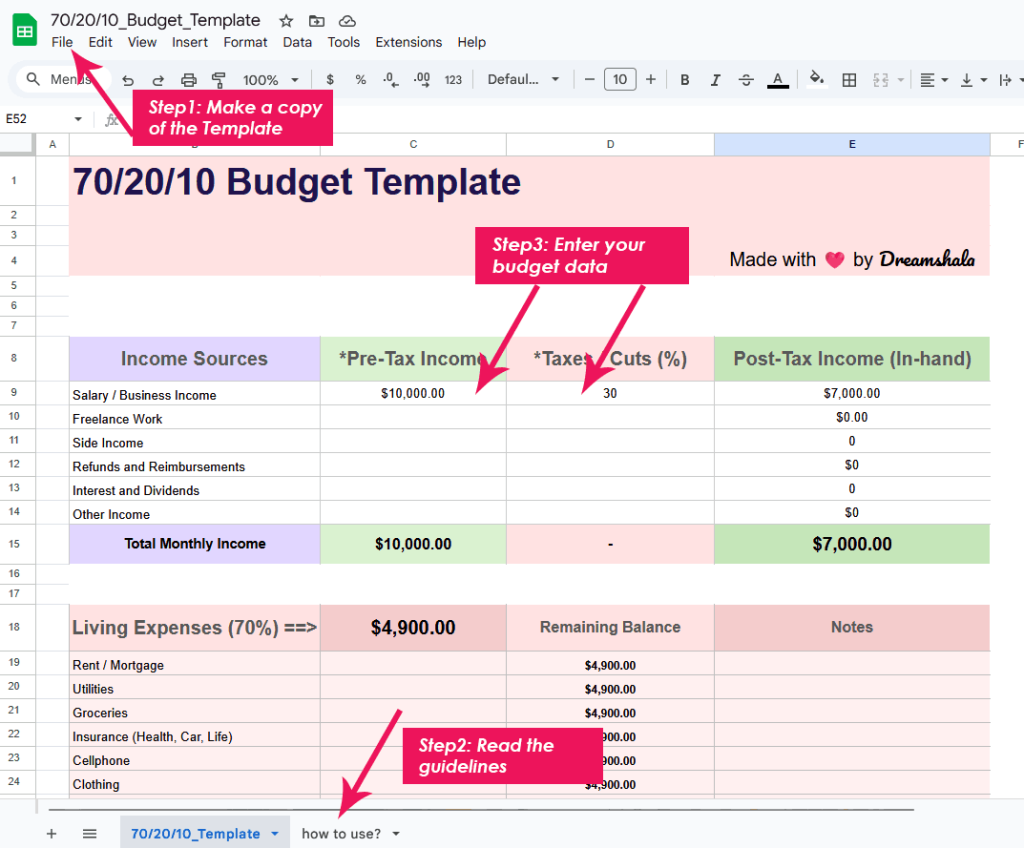

70/20/10 Budget – Google Sheets / MS Excel Template:

Access The 70/20/10 Budget Rule – Google Sheets/MS Excel Template here.

This Google Sheets / Excel Template is for those who want to plan and track their budget using their mobile, tablet, laptop, or computer.

This template is completely automatic.

You just need to open the template using the above link, save it as a copy, and start using it by entering your data in the respective input columns, as shown in the image below, and in the guidelines section in the template also.

Credit: Dreamshala

Don’t worry if you mistakenly enter data in the wrong fields and mess up the calculations.

You can always come back here and get a fresh copy of this template again and again.

So, don’t forget to Pin this article to your favorite Pinterest board now.

Happy budgeting.

Love from Dreamshala.

Popular Reads:

How To Make Money As A Teen: 19 Legit Ways

How To Make 10K A Month Fast? – 16 Easy Ways!

11 Realistic Ways To Make $20k a Month

Shruti Gupta is a freelance writer and SEO specialist with extensive experience covering online income opportunities, digital tools, and personal finance topics. Since 2020, she has written hundreds of articles focused on helping readers find reliable ways to earn money online, start side hustles, and grow their income streams. Through her work at Dreamshala, Shruti aims to provide well-researched, transparent, and actionable insights that help people make informed financial choices in the digital economy.