Do budgeting hacks mean cutting down on each of your wants and compromising your lifestyle till you save enough?

If yes, then you are wrong.

Budgeting means being intentional with your spending. In the long term, it tends to fulfill your financial goals without unnecessary compromise.

Thus, you won’t have to use a headband and sit with a headache at the end of the month, thinking of bills and why you don’t have any savings left.

I won’t speak any bookish theory, and being a human, I understand that real life is mostly unpredictable.

You never know when an unexpected expense can occur or an impulse purchase can ruin your finances for the month. This is true especially if you have debts or a low income.

So budgeting can never be perfect, but with simpler yet wiser approaches, you can start small and end up saving big.

With tiny habits, it becomes easy for you to be consistent even in the case of unpredictable expenses.

After a lot of trial-and-error, I have jotted down the most effective budgeting hacks below that are easier to stick with, irrespective of income, lifestyle, and expenses.

Even a few of the approaches mentioned here will make a significant difference. Let’s understand in detail!

Need Easy & Extra $300/Mo For Free?

Survey Junkie: Earn up to $50 per survey & a fixed $1.50 per referral. Sign up here.

Freecash: Get paid for taking surveys & testing apps. Earn up to a $250 signup bonus.

Swagbucks: Earn a $5 instant sign-up bonus & 10+ ways to earn real cash. Join now.

Branded Surveys: Paid over 35 Million. Earn up to $25 per survey. Sign up now.

Inbox Dollars: Get paid to watch videos. One has already made $75 within a week. $10 signup bonus.

Best Budgeting Hacks To Manage Finances

Do you know that Investopedia states that nearly 86% of people use budgeting regularly, but only 25% of them adhere to it?

While that sounds surprising, many people are unaware of how to do it effectively. Besides, for many, it is just tracking income and expenses, which is the biggest myth.

As of 2025, nearly 54% of Americans spent over four hours a week thinking about their finances. So while the hourly average wage of Americans lies between $29-$33, this time spent equals a loss between $116-$132 with no output.

But effectively spending the time can help you achieve financial goals.

Thus, careful budgeting is essential, and it’s not just jotting down where you spend, but your budget should not leave you with a question mark of how to pay bills or achieve financial goals.

As I have sailed in the same boat, spending hours daily on budgeting, I have covered the most effective hacks.

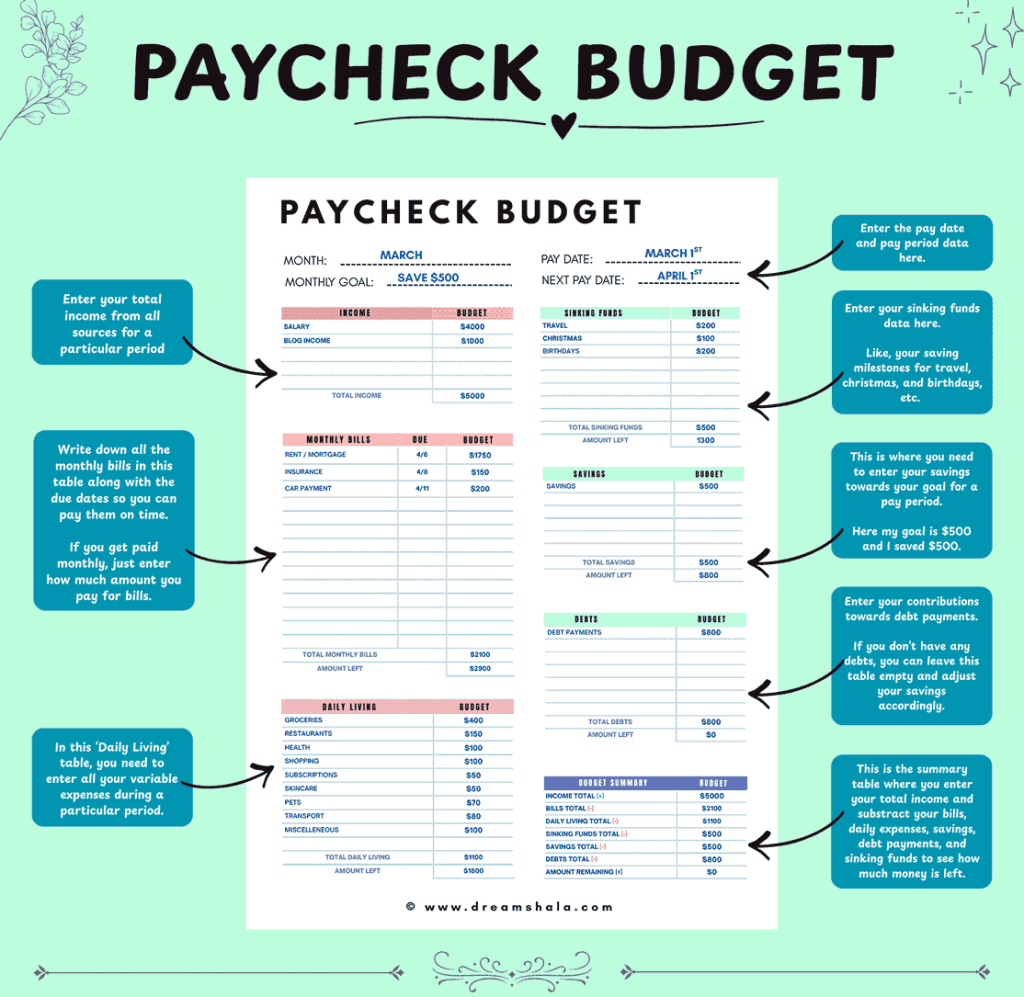

1. Create a New Budget For Every Paycheck

In case of low income, high expenses, or under miscellaneous circumstances, creating a monthly budget can feel complex. Here’s where you can start small, where you will make a new budget for every paycheck.

So if you get your paycheck weekly, biweekly, or once a month, then it helps to do so effectively. For ease, I am providing my free Paycheck Budget printable, which is a template that you can customize.

Let’s learn how to do so!

Credit: Dreamshala

In the initial stage, understand your income and expenses. So, check your bank statement for the previous month to analyze your take-home pay and where the penny is going monthly.

This is because it gives you a realistic idea of your income and spending habits. Accordingly, you can reduce your expenses to save money.

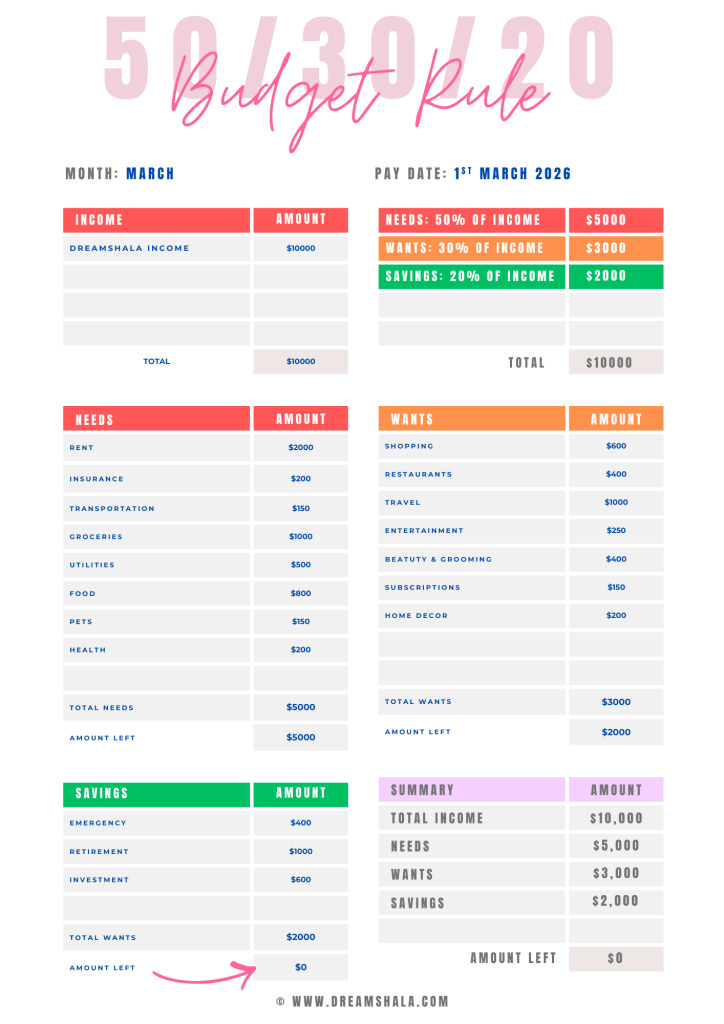

It had even helped me create a realistic budget to achieve my goals. The simplest method is to use the 50/30/20 budget rule, which breaks the expenses into three categories:

- 50% for your needs: You can use it for your basic needs like minimum debt payments, rent, utilities, groceries, commuting costs, etc.

- 30% for your wants: You can reserve 30% of your incoming pay for non-essentials and wants like restaurants, leisure activities, clothing, etc.

- 20% for your savings and debts: Allocate 20% for sinking funds, retirement plans, credit card debt, savings, contributions, etc. You can modify the amount and percentage based on your needs and financial goals.

For instance, if you live in an expensive area, then you will have to increase the percentage towards your needs, like rent, groceries, utilities, etc.

Accordingly, you will have to reduce your wants or savings as needed. Then it can become 70% needs, 10% wants, and 20% savings.

Read

70-20-10 Budget Rule – Complete Guide + Free Templates

50-30-20 Budget Rule: How to Make a Realistic Budget?

20 Best Free Money Hacks (Up To $1,000 Free Money)

2. Follow A Zero-based Budget

You can also follow a zero-based budget just like I do. It means plan your budget in such a way that no dollar is left unassigned after the categories end.

You should allocate all towards different categories.

This way, when you know you have nothing left, you spend less. So by the end of the month, you end up saving money, and instead of splurging on impulse buys, you spend it meticulously.

Read – How To Sell Printables on Etsy? – Complete Guide

3. Use Cash For The Things You Overspend On

Believe it or not, if you use a credit card, then you spend almost twice as much as the expenses you plan to pay with cash. It leads to unnecessary spending with credit cards.

To explain it better, science uses the concept of “the pain of paying”. When we buy anything, think of buying anything our mind activates the pain processing regions in our brain.

As credit cards have intangible cash, it reduces the pain of paying.

In comparison, when we pay with cash, we easily track our empty wallets and even watch them disappear, so we tend to spend less.

You might find it effortless to tap and pay, but its psychological impact increases your spending, which you don’t notice. So, control your spending habits and always use a cash-only budget. Thus, you can align with your financial goals.

But if you don’t find it feasible to use cash for all your needs, then use cash at places where you tend to overspend, or bills go higher than expected.

Some of the areas where you can use cash include:

- Clothing

- Restaurants

- Groceries

- Beauty and makeup

- Leisure and entertainment, etc

A simple rule is to analyze the specific areas of the category where you have to spend and withdraw a particular amount for each of them. Keep it reserved and spend it only on those categories.

For example, if you reserve $70 in an envelope for clothing, then that’s all you have. Don’t withdraw money from any other spending category and wait for your next payday to allocate more funds into clothing if needed.

Therefore, using cash envelopes for each category helps you to control your spending based on the budget. I personally use this approach, and it helps me save a lot.

More often, I feel like I should wait until next payday when I need to spend more, but till the time I realize that I don’t need to spend more, it was an impulsive decision.

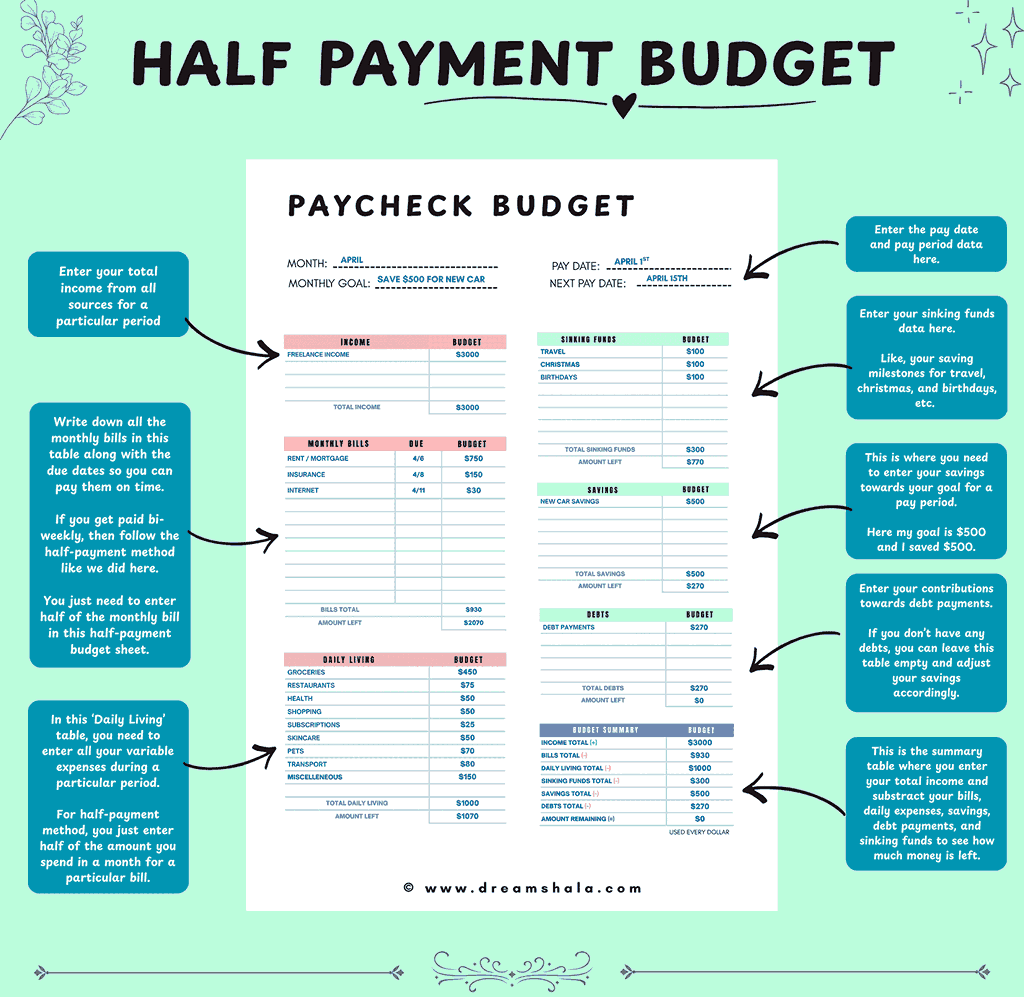

4. Follow the Half Payment Method for Big Expenses

Credit: Dreamshala

Even if I have lived days when I earned hand to mouth, and trust me, making ends meet before the paycheck becomes difficult. Here’s when I followed the half payment method after learning about it.

The half payment method means totaling your regular monthly bills and dividing them in half. So, if you have a payday twice a week, then use the payday funds and reserve the half-bill amount that you have to pay in the next bill.

So, when it’s time to pay the bill, you don’t have to allocate the entire bill amount from your current pay, but only half, as you would already have it from the previous one.

For example, if you pay $900 monthly for rental, then you should do the following:

- You have to reserve $450 from your paycheck, which you will receive for the period before the rental due.

- When you receive the paycheck for the period when rent is due, you just need to allocate $450 from that amount instead of the entire $900 in one go for the rental payment.

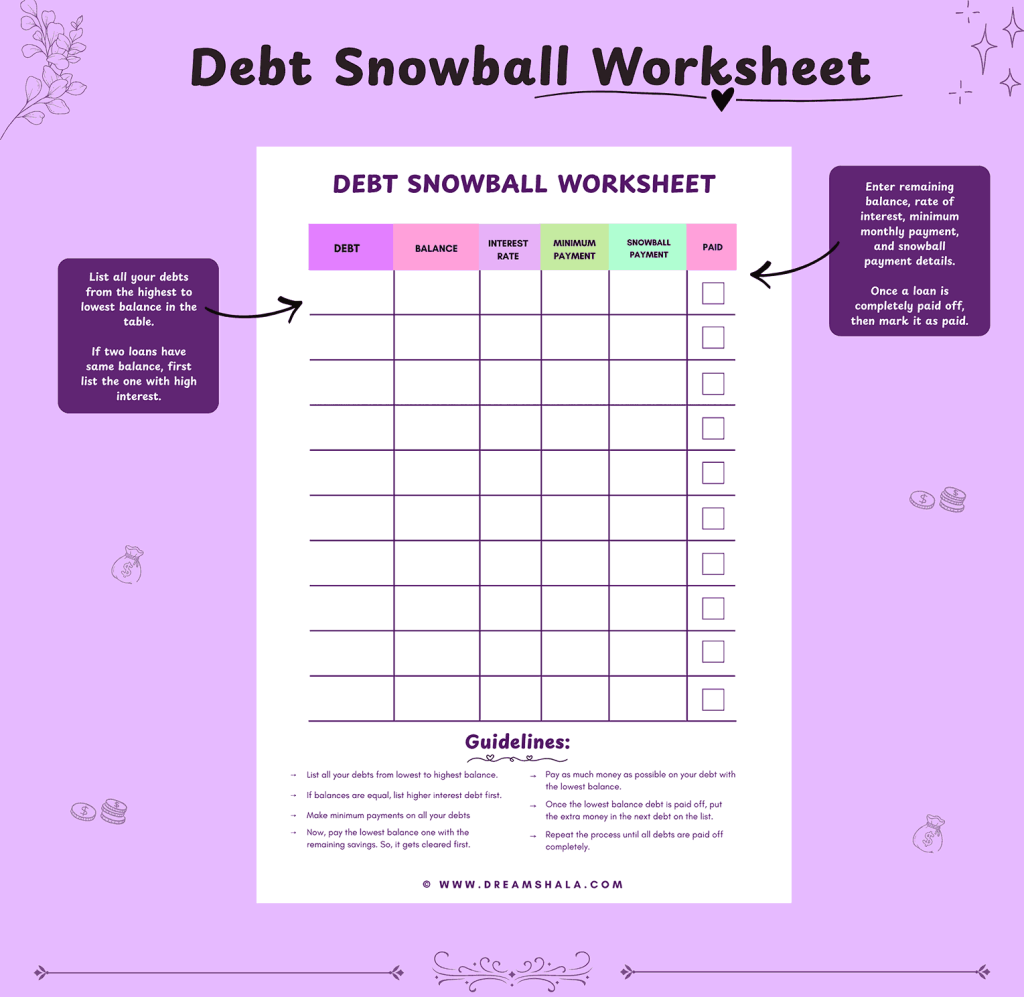

5. Clear Debts Using The Debt Snowball or Avalanche Method

You might have debts like a home loan, EMI, or any other, and the debt snowball method or the avalanche method is perfect for them.

For this, you have to select a debt payoff plan that suits your lifestyle and preferences.

The debt avalanche method explains that you should clear the one with the highest interest rate first. It is the fastest and most effective way to clear debt and save money on interest fees.

In the template that I am providing above, you have to list all the debts in order of their interest rates from largest to smallest.

Credit: Dreamshala

Next, prepare minimum payment plans for it, except for the debt that is most expensive as per the interest rate. Try to clear it as much as you can, and after that, you can follow the same approach for others as well, till you become debt-free.

In comparison, the debt snowball method aims to clear debts with the smallest amount first. It helps if you have a low income, need quick wins, and a fuel to stay consistent.

In the template given above, you should list all your debts in increasing order of balance. Pay the regular amount for all the debts except the one with priority. Next, pay as much as you can for the smallest debt.

Similarly, you can move to the next smallest debt till all of it is cleared. Irrespective of the methods you choose, ensure you don’t miss paying any debt’s minimum amount.

6. Practice The Power Of Pause

If you are a shopaholic like me, then I understand how regretful it is to stop yourself from buying what you want to. We convince ourselves with enough logic and emotional talks to be satisfied with our impulse purchases.

When we become impulsive about spending, we assume it’s easier for us to buy, and we need it at the moment. But we should become firm and ask ourselves the genuine need to buy it, and whether we be able to suffice without it.

Thus, we can analyze our spending triggers and the buying decisions we take impulsively. So, behaving with the power of pause helps as it blocks our impulsive spending habits and ensures that the expense aligns with the budget.

How To Practice The Power Of Pause

To practice the power of pause when you want to buy something, convince yourself, and wait for some time before buying. It is not applicable to needs, just for wants.

You should wait until you have a surplus of the purchase. The following are some of the time limits you can practice:

- For things in the range of $25, you can wait 24 hours before buying

- For purchases within the range of $50-$100, you should wait for at least 7 days

- For things between a decent amount of $100-$500, wait for a month before taking the step

Similarly, for amounts even higher than that, you should wait for 6 months to 1 year, and most likely you will realize you didn’t need it in reality.

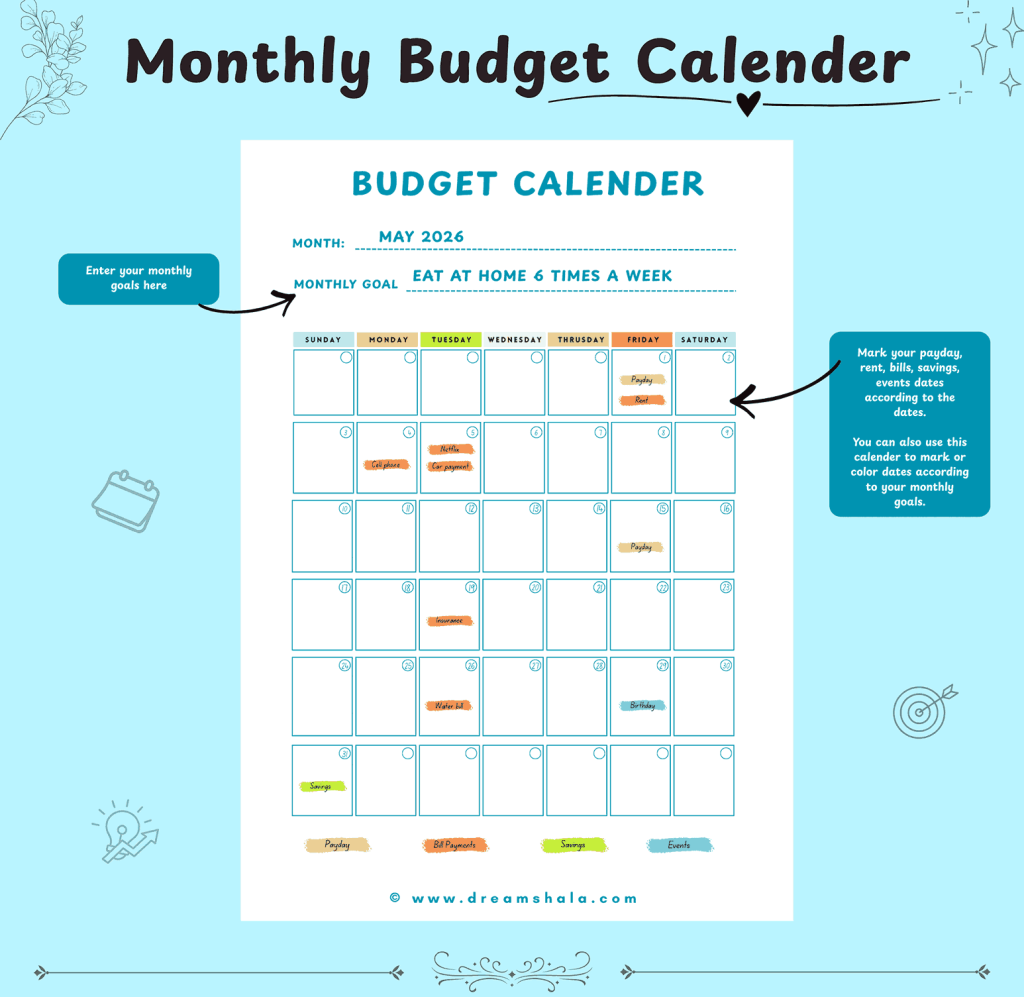

7. Use A Budget Calendar For Tracking Paydays and Bill Payments

For managing your finances and expenses better, you should use a budget calendar that’s specifically designed for the purpose. I personally use it and have designed my own for optimum effectiveness.

Credit: Dreamshala

The above budget calendar acts as a good visual cue to track paydays, when bills are to be paid, and expenses in the upcoming three months for planning accordingly.

With smart financial planning, it can help you build a good credit score, reduce impulse expenses, and motivate you to save money.

If you see your payday and your upcoming bill payments, then you will automatically think of spending less to cover expenses during that period and pay bills.

8. Set Frequent Budget Meetings

To ensure that you align with your budget and financial goals, set budget meetings with yourself or your partner at a fixed frequency. You can treat it like a money date, and this can be once a week, twice a week, once a month, or similar.

My preference is to listen to some retro songs while using my Budget Planner and then rewarding myself with some Netflix and ramen later.

Example of 50-30-20 budget rule with full budget allocation

With this approach, I can also modify my budget based on my needs throughout the month. The following are the things you should ensure in your budget meeting:

- Check how well your expenses are aligned with your budget and where you need to pay attention

- Focus on your dreams and saving goals that are feasible

- Review your expenses and cancel memberships that you don’t use

- Adjust the cash flow from. one category to another as needed

For example, if you overspend while shopping for groceries but have spent less on utilities, then you can move the utility funds towards groceries to adjust the misalignment.

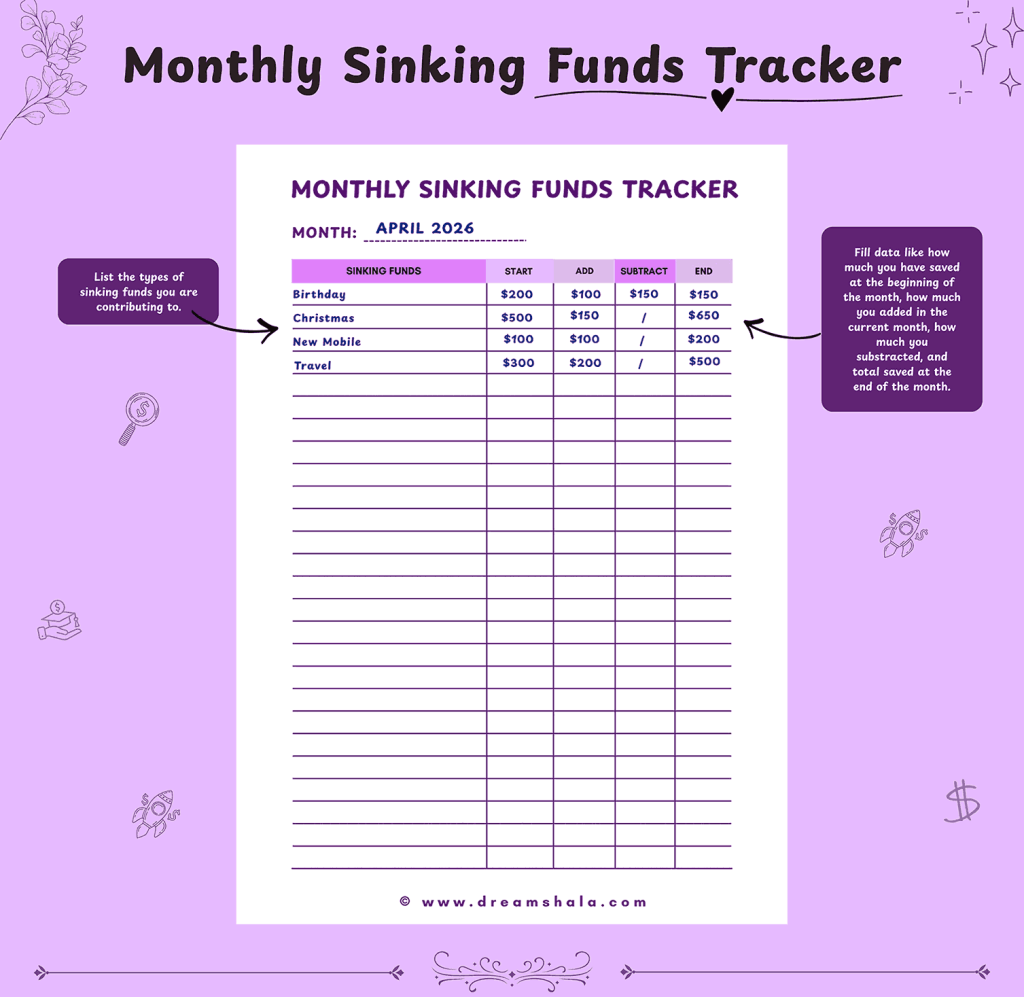

9. Use Sinking Funds For Saving Money

Sinking funds act as the best budgeting hacks for those having financial goals for planned expenditure.

For this, you should plan the known expenses and allocate a planned portion of money every month in their respective categories to use later.

Thus, sinking funds means future expenses for which you start allocating funds from your budget much in advance. It can be for anything, like going on a trip with friends, preparing to buy an HVAC, for your engagement, gifting, huge bills, etc.

The savings amount depends on your future expenses. In case you don’t know the cost, then you can start allocating an estimated fund every month till the expense occurs.

Credit: Dreamshala

The amount you need to save will be dependent on your goal.

When you know the amount, for example, you want to save, then divide it by the number of weeks/months you have in hand before buying, so you acquire sufficient funds till then.

In case you want to buy a PS5 costing $600 after three months, then save $200 every month for the purchase.

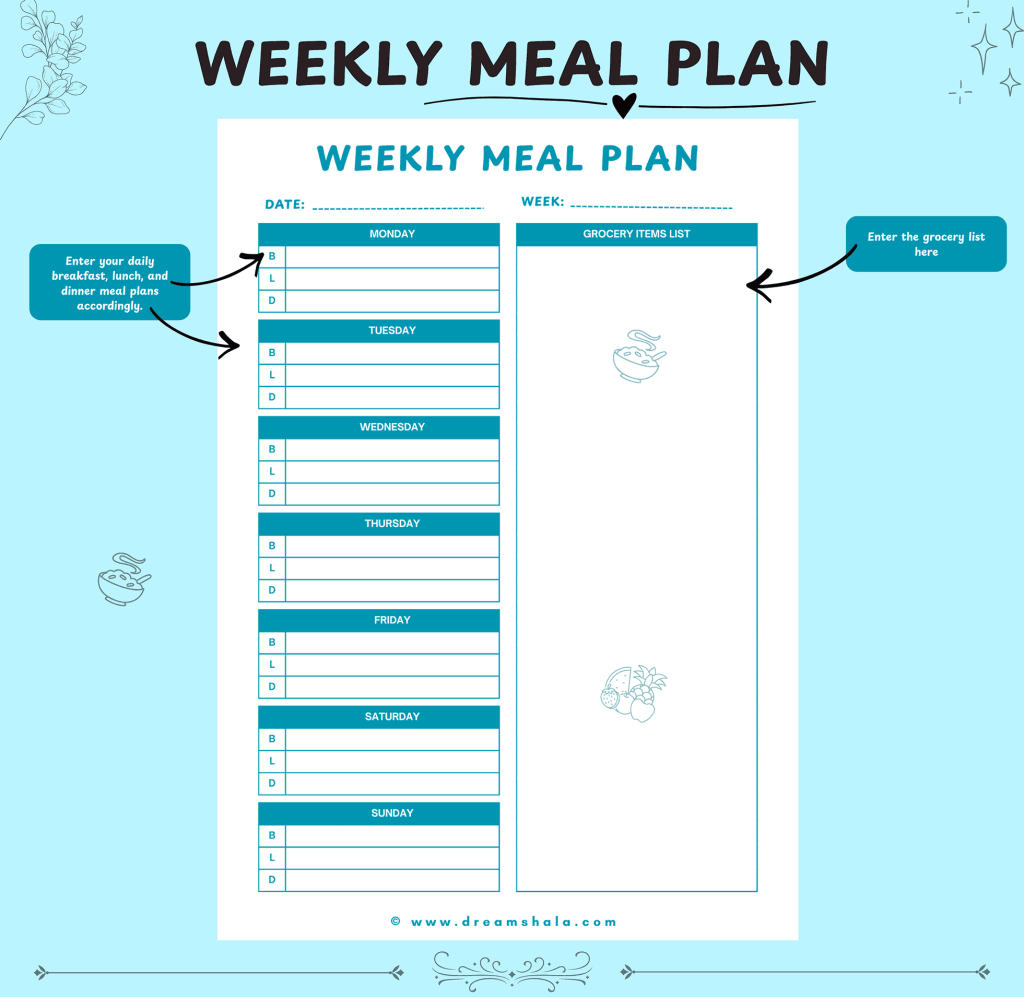

10. Meal Planning To Control Food Expenses

Food can be the costliest expenditure for many that they incur every month.

This is because of the ambiguity of what to cook, increased grocery expenses, or cravings, which often lead to unnecessarily eating out more than needed.

Here’s where I do proper planning, which helps me to ensure my meal is balanced and that my food budget is controlled as grocery prices increase every year.

Credit: Dreamshala

In a meal plan, you have to decide daily meals for each day of the week a week in advance.

You can also plan and allocate take-out days if needed. Accordingly, you can plan groceries, and you curb the need to buy extra or use the ones you already have.

The following are some wise tips that will help you adhere to the meal plan or plan for it;

- Check your refrigerator and pantry for meal ideas, as you might often find enough stuff that will save you from the need to go to the store.

- Use the available ingredients for optimum utilization of resources.

- Order your groceries from Instacart to curb your expenses in impulsive grocery shopping.

- Check grocery store flyers for sale items and accordingly do meal planning to save money.

- Chase easy meals like one-pot recipes, you won’t feel the need to go to a takeaway, and it will satisfy your cravings.

You can jot down your meal plan in the printable provided, and the nutritional intake and goals depend on you.

11. Learn to Curb Your Excess Wants And Focus On The Things That Matter

Personal finance is subjective for everyone, and there’s no one-size fit for all.

So, you are the controller of your finances. With a budget, you can smartly plan where your income will go. This way you don’t o have to sit with a headache towards the end of the month, figuring out where the money went.

Budgeting helps you analyze the amount you can spend for that particular month on needs, wants, sinking funds, debts, and savings based on your preferences.

Being a shopaholic earlier, I couldn’t resist myself from buying what I wanted despite my basic pay. Hence, I used to fulfill my wants without compromising, only to be empty-handed even before the month-end.

I got used to doing odd jobs to make ends meet, but I couldn’t manage my money.

For me, earning was a way through which I fulfilled the void of materialistic satisfaction in my life. But these never end. Always own only whatever is needed, or use only a maximum 20% of your income for it.

By spending less on parties and impulse buys, you stay focused, relaxed, have more money, and have a chance to live with freedom.

Budgeting Hacks – Conclusion

Many times, we buy things without even considering why we need them or what their use is. Hence, it is necessary to always carefully reconsider your decision logically.

Moreover, never indulge in any form of peer pressure or comparisons. People spend more than what they have just to present themselves as wealthy, but personality matters instead of expensive fashion.

Most wiser ones don’t buy many clothes, but build a capsule wardrobe without outfits and colors that can form various combinations which look classy and new. This way, you don’t end up wasting money on fast fashion, which doesn’t last long.

The most affluent ones lead a sober or mediocre life, while those with low income often end up living from paycheck to paycheck because their expenses are mostly for flaunting a luxury status. Never go above your budget and focus on what matters.

The budgeting hacks mentioned above will help you live debt-free, manage finances effectively, and yet save for wants and long-term goals.

Download my free Monthly Budget Printable now to manage your finances effectively and to fulfill financial goals.

Also Read:

How To Make 10K A Month Fast? – 16 Easy Ways!

How to Make $3000 Fast? 15 Guaranteed Ways Inside!

15 Easy Ways to Make Money By Doing Nothing

Shruti Gupta is a freelance writer and SEO specialist with extensive experience covering online income opportunities, digital tools, and personal finance topics. Since 2020, she has written hundreds of articles focused on helping readers find reliable ways to earn money online, start side hustles, and grow their income streams. Through her work at Dreamshala, Shruti aims to provide well-researched, transparent, and actionable insights that help people make informed financial choices in the digital economy.